NH Medicare Advantage Plans 2026 offer a comprehensive guide to the history, evolution, and current offerings of these plans. Delving into the nuances of these programs, this guide aims to provide readers with a clear understanding of the different types of plans available, their benefits and limitations, and the enrollment process. By the end of this journey, readers will be equipped with the knowledge to make informed decisions about their Medicare coverage.

This guide will explore the various types of Medicare Advantage Plans offered in 2026, including HMO, PPO, Private Fee-for-Service, and Special Needs Plans. We’ll delve into the key features and benefits of each plan, discussing out-of-pocket maximums, deductibles, and copays, as well as how these plans cover prescription medications, dental, and vision care.

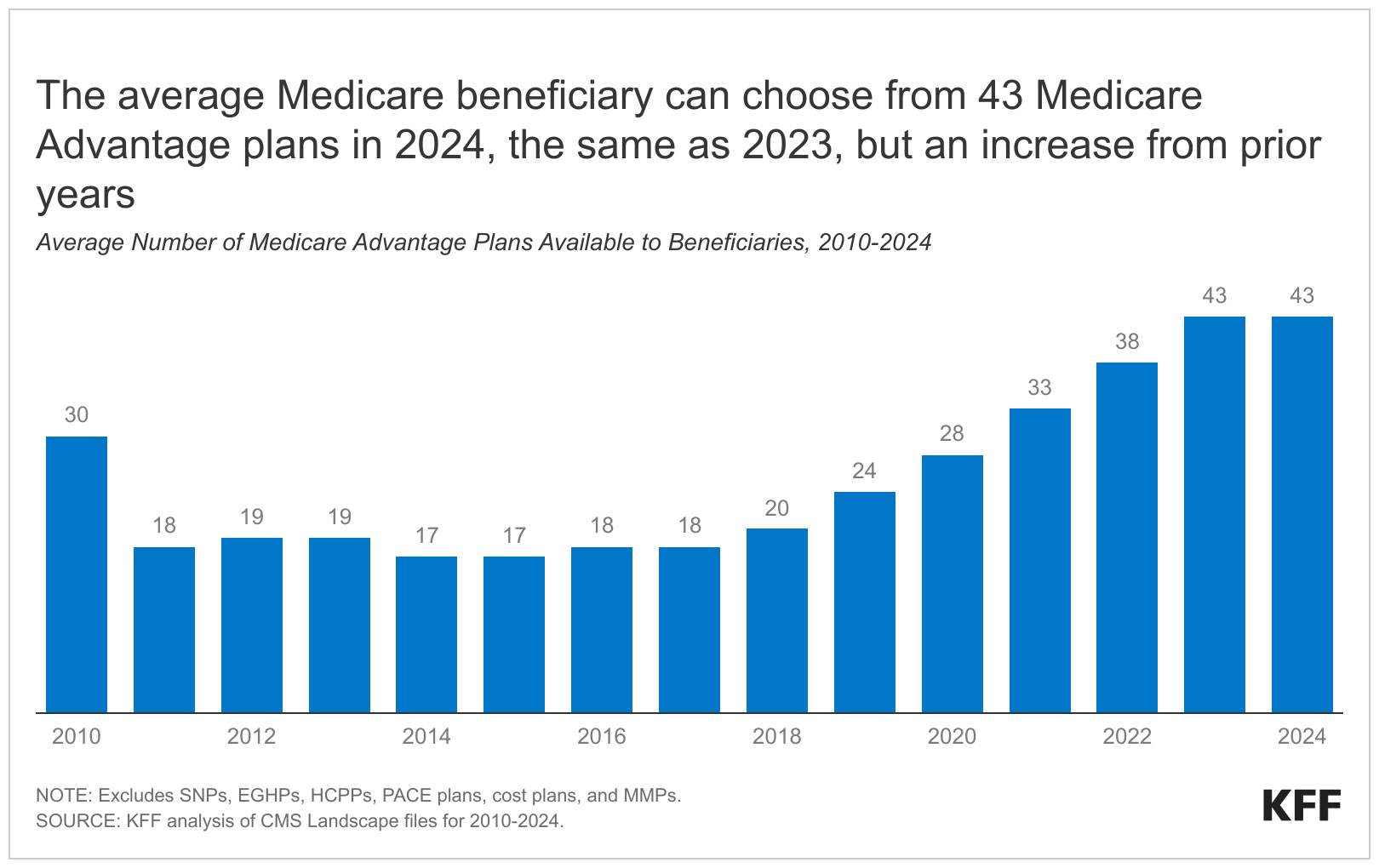

Overview of Medicare Advantage Plans for 2026.

In the shadows of the US healthcare landscape, Medicare Advantage plans silently evolved over the years, adapting to the ever-changing needs of American citizens. Since its inception in 2003, this innovative program has been slowly but surely transforming the way seniors and individuals with disabilities access healthcare services. With its roots in the Medicare Modernization Act, the Medicare Advantage program aimed to provide an alternative to traditional Medicare coverage, offering a more comprehensive and cost-effective approach to healthcare.

The Evolution of Medicare Advantage Plans

In its early days, the Medicare Advantage program was met with skepticism by many, who saw it as a mere addition to the existing Medicare system. However, over the years, it has grown into a robust and diverse program, offering a wide range of plans that cater to the varying needs of its beneficiaries. From Health Maintenance Organizations (HMOs) to Preferred Provider Organizations (PPOs), Medicare Advantage plans have become increasingly complex, with each offering unique features and benefits. As the healthcare landscape continues to shift, it’s essential to understand the evolution of Medicare Advantage plans to make informed decisions about one’s healthcare coverage.

- 1990s: Medicare Modernization Act passes, laying the groundwork for Medicare Advantage plans.

- 2003: Medicare Advantage plans become available to seniors and individuals with disabilities.

- 2009: Medicare Advantage plans undergo significant changes, including expanded benefits and increased funding for certain plans.

- 2015: Medicare Advantage plans begin to focus more on primary care and preventive services.

- 2020: Medicare Advantage plans expand their reach, offering benefits such as dental, vision, and hearing coverage.

Types of Medicare Advantage Plans in 2026

As Medicare Advantage plans continue to evolve, the types of plans available also change. In 2026, beneficiaries can choose from a variety of plans, including:

- Health Maintenance Organizations (HMOs): HMOs offer a network of healthcare providers and facilities that beneficiaries can use to receive services. These plans often require referrals from a primary care physician before seeing a specialist.

- Preferred Provider Organizations (PPOs): PPOs offer a network of healthcare providers and facilities that beneficiaries can use to receive services. These plans often charge lower rates for services received within the network and offer higher rates for services received outside the network.

- Private Fee-for-Service (PFFS) Plans: PFFS plans allow beneficiaries to choose any healthcare provider or facility that accepts the plan’s payment terms.

- Cost Plans: Cost plans allow beneficiaries to receive Medicare-covered services from any healthcare provider or facility, but they must pay the healthcare provider directly.

Specialized Medicare Advantage Plans in 2026

In addition to the traditional types of Medicare Advantage plans, there are also specialized plans that cater to the unique needs of certain beneficiaries. These plans include:

- Special Needs Plans (SNPs): SNPs are Medicare Advantage plans that cater to beneficiaries with special needs, such as those with chronic conditions or disabilities.

- Dual Eligible Special Needs Plans (D-SNPs): D-SNPs are Medicare Advantage plans that cater to beneficiaries who are dually eligible for Medicare and Medicaid.

- Chronic Special Needs Plans (C-SNPs): C-SNPs are Medicare Advantage plans that cater to beneficiaries with chronic conditions, such as diabetes or heart disease.

Types of NH Medicare Advantage Plans Offered in 2026.

In the mysterious realm of healthcare, the veil has been lifted, uncovering four enigmatic types of NH Medicare Advantage Plans. As 2026 approaches, it’s essential to navigate these plans, each with its unique set of benefits and limitations. Let us embark on this journey of discovery, delving into the heart of each plan type.

HMO (Health Maintenance Organization) Plans

HMO plans are shrouded in mystery, but their allure lies in their comprehensive coverage and affordable premiums. As you delve deeper into these plans, you’ll find that they offer a wide range of benefits, including:

- Routine check-ups and preventive care

- Prescription medications

- Surgical procedures

- Hospital stays

However, beware of the fine print, for HMO plans often come with a catch. You’ll be required to choose a primary care physician and receive referrals from them for specialist care. This might seem restrictive, but some find it a valuable trade-off for the lower premiums.

PPO (Preferred Provider Organization) Plans

PPO plans, on the other hand, operate within a network of providers, but you have the freedom to venture outside this realm, albeit at a higher cost. This flexibility appeals to those who value optionality, but be aware that PPO plans tend to have higher premiums compared to HMOs.

| Plan Type | Coverage Level | Premiums | Network Providers |

|---|---|---|---|

| HMO | Comprehensive | Lower | Restricted |

| PPO | Comprehensive | Flexible |

Private Fee-for-Service (PFFS) Plans

PFFS plans operate in a realm of mystery, where providers are paid on a fee-for-service basis. This creates a complex situation, as the plans may have varying levels of coverage and premiums. It’s essential to scrutinize the fine print, as some PFFS plans might offer inadequate coverage or high costs.

Beware, for PFFS plans can be a tangled web of complexity.

Special Needs Plans (SNPs)

SNPs are designed for those with specific, chronic conditions, such as diabetes or heart failure. These plans offer tailored coverage and support, but come with stricter guidelines and rules. It’s essential to carefully evaluate whether an SNP is the right fit for your needs.

SNPs are a lifeline for those navigating the complexities of chronic conditions.

Key Features and Benefits of NH Medicare Advantage Plans.

Medicare Advantage Plans in New Hampshire for 2026 offer a diverse range of benefits and features that cater to the unique needs of seniors and individuals with disabilities. These plans combine the convenience of a single insurance plan with the comprehensive coverage of Original Medicare.

To understand the value of Medicare Advantage Plans, it’s essential to consider the key features and benefits that set them apart from other healthcare options. One of the most significant advantages of these plans is the emphasis on preventive care, which can help individuals detect and manage health issues before they become more complex and costly.

Out-of-Pocket Maximums, Deductibles, and Copays

Medicare Advantage Plans in NH for 2026 typically come with out-of-pocket maximums, which limit the amount individuals must pay for healthcare services and prescription medications. This feature helps to prevent surprise medical bills and provides peace of mind for those who worry about healthcare costs.

For example, some Medicare Advantage Plans in NH for 2026 have out-of-pocket maximums as low as $3,000.

In addition, deductibles and copays play a crucial role in determining the overall cost of healthcare services. Medicare Advantage Plans often have lower deductibles and copays compared to Original Medicare, making it easier for individuals to afford necessary care.

According to the Centers for Medicare and Medicaid Services (CMS), Medicare Advantage Plans often have lower copays for doctor visits and hospital stays compared to Original Medicare.

5 Benefits of Medicare Advantage Plans

The following benefits are among the most significant advantages of Medicare Advantage Plans:

- Comprehensive coverage that includes all services provided by Original Medicare, plus additional benefits such as dental and vision care. This means that individuals can receive comprehensive care without the hassle of navigating multiple plans and claims.

- Preventive care is emphasized, which helps to detect and manage health issues before they become more complex and costly.

- Lower out-of-pocket costs compared to Original Medicare, including lower deductibles and copays.

- A wider network of healthcare providers, including specialist and primary care physicians.

- Additional benefits, such as fitness programs and healthy food discounts, that promote overall well-being and reduce healthcare costs.

5 Drawbacks of Medicare Advantage Plans

While Medicare Advantage Plans offer numerous benefits, they also come with some drawbacks:

- Network restrictions that may limit access to healthcare providers, particularly if individuals have a preferred doctor or specialist.

- Higher costs for out-of-network services, which can lead to unexpected medical bills.

- Some plans may have more restrictive coverage for certain services, such as mental health treatment or physical therapy.

- Additional fees for services not covered by the plan, such as prescription medications or hospital stays.

- Complexity in comparing plan benefits and costs, which can lead to confusion and mismanagement of healthcare expenses.

Coverage of Prescription Medications, Dental, and Vision Care

Medicare Advantage Plans in NH for 2026 often provide comprehensive coverage for prescription medications, including generic and brand-name drugs. Some plans may have formularies that restrict coverage for certain medications, while others may have higher copays for expensive medications.

For example, some Medicare Advantage Plans in NH for 2026 may have a $10 copay for generic medications and a $35 copay for brand-name medications.

Additionally, Medicare Advantage Plans often cover dental and vision care, including routine check-ups and corrective lenses. Some plans may have additional coverage for hearing aids and other assistive devices.

According to the CMS, Medicare Advantage Plans may cover 100% of the costs associated with routine dental cleanings, fillings, and extractions.

When choosing a Medicare Advantage Plan, it’s essential to carefully review the benefits and costs to determine which plan best meets your healthcare needs and budget.

How to Enroll in a New Hampshire Medicare Advantage Plan in 2026.

In the mystical realm of Medicare, where choices and options abound, navigating the process of enrolling in a New Hampshire Medicare Advantage Plan can be a daunting task. As the clock ticks closer to 2026, it’s essential to comprehend the intricacies of this process, ensuring a smooth transition into a plan that suits your needs.

The Role of Original Medicare and Medicare Supplement Insurance

——————————————————–

In the world of Medicare, Original Medicare and Medicare Supplement Insurance (Medigap) play distinct yet interconnected roles. Original Medicare, consisting of Part A (hospital insurance) and Part B (medical insurance), provides a foundation for health coverage. Medigap, on the other hand, serves as a supplement to Original Medicare, filling in the gaps left by the latter. When pairing a Medicare Advantage Plan with Original Medicare and Medigap, it’s crucial to comprehend the relationships between these components.

- Original Medicare covers hospital and medical costs, but has a Part D gap for prescription drugs.

- Medicare Supplement Insurance (Medigap) fills in the gaps left by Original Medicare, covering costs such as copayments, coinsurance, and deductibles.

- A Medicare Advantage Plan combines the benefits of Original Medicare with additional perks, such as vision, dental, and fitness programs.

Annual Enrollment Period (AEP) and Its Timeline

———————————————–

Imagine wandering through a vast forest, where ancient trees stand tall, representing the Medicare Advantage Plans available in New Hampshire. The Annual Enrollment Period (AEP) serves as a crucial landmark in this journey, offering a window of opportunity to reassess and adjust your coverage. This period, typically spanning from mid-October to mid-December, provides a fleeting moment to make changes to your Medicare Advantage Plan.

Meeting the Eligibility Criteria

As the clock strikes midnight on September 30th, the Annual Enrollment Period commences, and with it, a host of requirements must be met to ensure eligibility. These conditions vary across each plan, but generally include:

- Aged 65 or older, or have a qualifying disability, or have end-stage renal disease (ESRD), or have amyotrophic lateral sclerosis (ALS).

- Currently enrolled in Medicare Part A and Part B.

- Reside in the service area of the selected Medicare Advantage Plan.

Enrollment Process

As you step into the mystical realm of Medicare enrollment, a winding path emerges before you. To embark on this journey, follow these steps:

- Contact the Centers for Medicare and Medicaid Services (CMS) or a licensed insurance agent for guidance.

- Review your existing Medicare coverage and identify areas for improvement.

- Research and compare Medicare Advantage Plans in New Hampshire.

- Consult with a licensed insurance agent or the plan vendor to determine the eligibility criteria.

- Submit your application during the Annual Enrollment Period (AEP), between October 15th and December 7th.

Evaluating the Performance of NH Medicare Advantage Plans.

Evaluating the performance of New Hampshire Medicare Advantage (MA) plans is crucial for consumers to make informed decisions about their healthcare coverage. With numerous plans available, each with unique features and benefits, comparing performance metrics is essential to ensure that beneficiaries receive high-quality care. Quality ratings and performance metrics provide valuable insights into a plan’s ability to deliver effective and compassionate care, which is critical for maintaining good health and addressing complex medical conditions.

Evaluating quality ratings involves assessing the performance of plans across various domains, including clinical effectiveness, patient satisfaction, and health outcomes. These metrics are often reported by the Centers for Medicare and Medicaid Services (CMS) as part of the Overall Star Rating system, which rates plans on a scale of one to five stars.

Quality Ratings and Performance Metrics.

CMS employs a comprehensive evaluation framework to assess the performance of MA plans, focusing on key quality metrics such as:

- Hospital readmission rates:

- ER visits:

- Hospitalizations:

- Mortality rates.

- Patient satisfaction metrics:

- Health outcomes:

These rates indicate the likelihood of a patient being readmitted to the hospital within a short period after discharge, which can be an indicator of the quality of care provided.

Frequent ER visits can signify inadequate access to primary care or inadequate management of chronic conditions.

The number of hospitalizations can be an indicator of the effectiveness of care provided by the plan.

These metrics evaluate the overall satisfaction of patients with the care they receive, including their experiences with provider communication, care coordination, and access to care.

Metrics such as blood pressure control, blood sugar management, and cancer screening rates help assess the effectiveness of care in managing chronic conditions and promoting good health.

These metrics are used to calculate the Overall Star Rating, which reflects a plan’s performance across various domains. A higher rating indicates better performance and a higher level of care.

Analyzing Plan Performance.

Consumers can access and compare plan performance metrics through the CMS website, where they can:

* Search for plans in their area and view their star ratings.

* Compare plan performance metrics across various domains.

* Evaluate plans based on their overall star ratings and individual metrics.

* Access plan-level data to make informed decisions about their coverage.

By examining these metrics, consumers can make more informed decisions about their healthcare coverage and ensure that they choose a plan that meets their needs and provides high-quality care.

Consumer Engagement and Transparency.

The CMS website provides a user-friendly interface for consumers to analyze plan performance and make informed decisions about their coverage. By making this information readily available, consumers are empowered to engage with their healthcare providers and plans, promoting a more transparent and accountable healthcare system.

Addressing Common Concerns about NH Medicare Advantage Plans.: Nh Medicare Advantage Plans 2026

In the mystifying world of healthcare, numerous concerns and misconceptions surround New Hampshire Medicare Advantage Plans. Like a shroud of uncertainty, these doubts can obscure the truth, leaving beneficiaries bewildered. Let us lift the veil and dispel these myths, revealing the facts and benefits of NH Medicare Advantage Plans.

Myths and Misconceptions

Medicare Advantage Plans have been shrouded in mystery, with many beneficiaries harboring misconceptions. For instance, some believe that these plans do not cover essential services, while others think they are more expensive than traditional Medicare. However, these claims are as unfounded as a ghostly whisper. In reality, NH Medicare Advantage Plans offer a wide range of services, including doctor visits, hospital stays, and prescription medications, often at a lower cost than traditional Medicare.

Handling Long-Term Care and Home Healthcare Services

A common concern surrounds the provision of long-term care and home healthcare services. Like a puzzle piece, these services need to fit seamlessly into the Medicare Advantage framework. Fortunately, NH Medicare Advantage Plans have stepped up to the plate, offering a range of options for beneficiaries requiring long-term care and home healthcare services. From in-home care to assisted living facilities, these plans provide the necessary support for individuals with chronic illnesses or disabilities.

The Appeal and Grievance Process for Disenrolled Beneficiaries, Nh medicare advantage plans 2026

The disenrollment process can be as treacherous as a mysterious labyrinth, with beneficiaries unsure of their next steps. However, the appeal and grievance process offers a lifeline, allowing disenrolled beneficiaries to challenge their decisions. Like a beacon of hope, the appeal and grievance process provides a structured framework for beneficiaries to have their concerns heard and addressed. By understanding this process, beneficiaries can navigate the complex landscape of NH Medicare Advantage Plans with confidence.

Medicare Advantage Plans are designed to provide comprehensive coverage, including long-term care and home healthcare services.

Tips for Beneficiaries

To navigate the complex world of NH Medicare Advantage Plans, beneficiaries should:

- Familiarize themselves with the plan’s benefits and limitations

- Understand the appeal and grievance process

- Seek guidance from licensed insurance agents or brokers

- Take advantage of free resources, such as the Medicare.gov website

By following these tips, beneficiaries can make informed decisions and ensure they receive the care they need, without getting lost in the labyrinth of NH Medicare Advantage Plans.

Accessing Healthcare Services with NH Medicare Advantage Plans

Accessing healthcare services is a crucial aspect of Medicare Advantage plans in New Hampshire. With numerous plan options available, understanding the network provider options, in-network and out-of-network care costs, and alternative payment models can help individuals navigate their healthcare needs effectively.

In the state of New Hampshire, Medicare Advantage plans are offered by various insurance companies, each with its own network of healthcare providers. Two common types of plans are HMO (Health Maintenance Organization) and PPO (Preferred Provider Organization).

Network Provider Options: HMO vs. PPO

The primary difference between HMO and PPO plans lies in their network provider options. HMO plans typically require members to choose a primary care physician (PCP) who coordinates their care and refers them to specialists within the HMO network. This approach helps to reduce costs and streamline care. On the other hand, PPO plans offer a broader network of providers, allowing members to visit specialists without a referral. However, PPO plans often come with higher premiums compared to HMO plans.

In New Hampshire, several Medicare Advantage plans offer both HMO and PPO options, enabling individuals to choose the plan that best suits their healthcare needs.

In-Network vs. Out-of-Network Care Costs

Understanding the difference in care costs between in-network and out-of-network providers is crucial when accessing healthcare services with Medicare Advantage plans. In-network providers have a contractual agreement with the health insurance company, which typically results in lower costs for services. Out-of-network providers, however, may charge higher rates for the same services. It’s essential for individuals to check their plan’s network provider list and understand the costs associated with in-network and out-of-network care before making any medical decisions.

A hypothetical example illustrates the difference in costs:

Suppose an individual has an HMO plan with a $500 copayment for doctor visits. If they see an in-network doctor, the copayment applies. However, if they see an out-of-network doctor, the copayment may be higher, or the insurance company might not cover part of the costs, resulting in higher out-of-pocket expenses.

Alternative Payment Models (APMs) and Accountable Care Organizations (ACOs)

In an effort to improve healthcare outcomes and reduce costs, Medicare Advantage plans in New Hampshire often incorporate alternative payment models (APMs) and accountable care organizations (ACOs). These innovative models focus on coordinating care and sharing savings among healthcare providers.

APMs, such as value-based payment arrangements, encourage healthcare providers to prioritize quality care over quantity. For example, a value-based payment model might reimburse doctors based on the patient’s health outcomes rather than the number of procedures performed.

ACOs, on the other hand, are groups of healthcare providers that work together to coordinate care and share financial responsibility for their patients. By collaborating and sharing best practices, ACOs can improve patient outcomes and reduce healthcare costs.

For instance, a hypothetical ACO in New Hampshire might include primary care physicians, specialists, hospitals, and other healthcare providers who work together to coordinate patient care. By sharing data and expertise, this ACO can identify areas for improvement and implement evidence-based practices to enhance patient outcomes.

By leveraging APMs and ACOs, Medicare Advantage plans in New Hampshire aim to provide high-quality, patient-centric care while reducing costs and improving healthcare outcomes for their members.

Conclusion

NH Medicare Advantage Plans 2026 are a vital component of healthcare coverage for millions of Americans. By understanding the ins and outs of these plans, readers can make informed decisions about their Medicare coverage, ensuring they receive the best possible care. Whether you’re a seasoned Medicare expert or just starting your journey, this guide has provided a wealth of information to aid you in navigating the complexities of Medicare Advantage Plans.

General Inquiries

What is the difference between HMO and PPO Medicare Advantage Plans?

HMO (Health Maintenance Organization) and PPO (Preferred Provider Organization) Medicare Advantage Plans differ in their network provider options and out-of-network care costs. HMO plans typically require patients to see in-network providers, while PPO plans allow patients to see out-of-network providers at a higher cost.

How do Medicare Advantage Plans cover prescription medications?

Medicare Advantage Plans may cover prescription medications through a pharmacy network or a separate prescription drug plan. Some plans may also offer coverage for generic medications or brand-name medications at a lower cost.

Can I enroll in a Medicare Advantage Plan if I have a chronic health condition?

Yes, you can enroll in a Medicare Advantage Plan with a chronic health condition. Many plans offer specialized coverage for conditions such as diabetes, heart disease, and cancer.