Kicking off with 457b 2026 contribution limits, this topic is crucial for maximizing your retirement savings. With the significance of 457(b) plans and the consequences of not contributing at maximum limits by 2026, it’s essential to understand the advantages of utilizing these limits and the potential risks of missing out on opportunities.

The process for identifying your employer’s plan and the contribution limits that apply to your individual account is straightforward. By understanding the tax implications for participants and the benefits of participating in 457(b) plans, you can create a comprehensive retirement savings strategy. We’ll also explore the proposed changes to 457(b) contribution limits for 2026 and how they impact individual participant accounts.

Overview of 457(b) 2026 Contribution Limits and Their Impact on Retirement Savings

The 457(b) plan is a valuable retirement savings vehicle for government employees and tax-exempt organizations. These plans allow participants to contribute a portion of their income on a pre-tax basis, reducing their taxable income and increasing the amount available for retirement savings. However, the contribution limits for 457(b) plans have been increasing over the years, and by 2026, the limits will have significantly changed.

If you fail to contribute at the maximum limits by 2026, you risk missing out on significant tax savings and a more substantial retirement nest egg. As you’ll see below, contributing at the maximum limits can lead to a substantial increase in your retirement savings, making it a crucial decision for those eligible for 457(b) plans.

Advantages of Utilizing 457(b) Contribution Limits

The 457(b) plan offers several advantages that make it an attractive option for retirement savings. Firstly, the contribution limits are higher than those of 401(k) and 403(b) plans, allowing individuals to save more for retirement. Additionally, the plan allows catch-up contributions for individuals aged 50 and above, enabling them to save even more.

* The 457(b) plan allows contributions of up to $20,500 in 2026, with an additional $6,500 in catch-up contributions for individuals aged 50 and above.

* Contributions to a 457(b) plan are made on a pre-tax basis, reducing taxable income and increasing the amount available for retirement savings.

* Employers may also contribute to a 457(b) plan, providing additional funds for the individual’s retirement.

Implications of Employer-Matched Contributions

Employer-matched contributions can significantly impact the overall retirement savings strategy. When an employer matches an individual’s contributions, it effectively increases the individual’s retirement savings by up to 100%. This can be a game-changer for individuals who are struggling to save for retirement or those who are looking to accelerate their retirement savings.

* Employer matching contributions can be up to 100% of the individual’s contributions, depending on the employer’s policy.

* Employers may also have different matching formulas, such as 50% of the first 6% of contributions or 100% of the first 3% of contributions.

* Employees should take advantage of employer matching contributions to maximize their retirement savings.

Effects of Income Level on Contribution Limits

The income level of an individual can have a significant impact on their contribution limits to a 457(b) plan. In 2026, the contribution limit is $20,500, but individuals with higher incomes may be subject to the 457(b) plan’s income cap. This means that individuals with incomes above a certain threshold may not be able to contribute to a 457(b) plan or may be limited in their contribution amount.

* The 457(b) plan’s income cap is $100,500 for 2026.

* Individuals with incomes above the income cap may be subject to a reduced contribution limit.

* Employees should consult with their HR representative or a financial advisor to determine the impact of their income level on their contribution limits.

Importance of Planning Ahead

Planning ahead is crucial when it comes to retirement savings. Individuals should aim to contribute at the maximum limits to their 457(b) plan to maximize their retirement savings. With the income cap and catch-up contribution limits in place, individuals should plan accordingly to ensure they are making the most of their retirement savings.

* Individuals should contribute at the maximum limits to their 457(b) plan to maximize their retirement savings.

* Employees should also take advantage of catch-up contributions to accelerate their retirement savings.

* Individuals should consult with a financial advisor to determine the best strategy for their retirement savings.

Understanding the 457(b) Plan Contribution Limits for 2026

In the realm of retirement savings, 457(b) plans offer a robust option for employees to contribute to their future financial security. For the year 2026, it’s essential to grasp the contribution limits and tax implications involved in these plans.

To start, an individual must first understand which 457(b) plan they’re eligible for. This usually involves identifying the employer’s plan and determining the contribution limits that apply to their personal account. Typically, employers administer 457(b) plans, and participants must adhere to the guidelines set forth by their employer’s plan.

### Identifying Your Employer’s 457(b) Plan

* The plan administrator will determine the contribution limits for each plan. You can usually find this information on the employer’s website or by contacting the plan administrator directly.

* Some common features of 457(b) plans include:

* Employer-matched contributions

* Vesting schedules

* Loan provisions

* Required minimum distributions upon retirement

### Understanding Tax Implications

* Contributions to 457(b) plans are made on an after-tax basis, which means you’ve already paid income tax on the funds before contributing to the plan.

* However, qualified distributions are tax-free, as they’re considered part of your retirement income.

* This tax-free treatment can lead to significant tax savings over the long term.

### Examples of Employers Offering 457(b) Plans

* Public schools and school districts

* Government agencies

* Higher education institutions

* Healthcare organizations

* Local municipalities and counties

These employers often offer 457(b) plans as a benefit to their employees, allowing them to save for retirement while reducing their taxable income.

### Potential Risks Associated with High Contribution Rates

* While contributing to a 457(b) plan can be beneficial, high contribution rates may put a strain on your current financial situation.

* It’s essential to create a retirement savings plan that balances your short-term goals with your long-term objectives.

### Common Features of 457(b) Plans

* Employer-matched contributions: Some employers offer matching contributions to encourage employees to participate in the plan.

* Vesting schedules: Employer contributions may be subject to a vesting schedule, which means you must work for the employer for a certain period before you can keep the contributions.

* Loan provisions: Participants can often borrow from their 457(b) plan, but this may impact the plan’s performance and tax implications.

* Required minimum distributions: Upon retirement, participants must take minimum distributions from their 457(b) plan, which can impact tax liability.

Changes to 457(b) Contribution Limits in 2026 and Their Effect on Individual Participants

The 457(b) plan has long been a popular option for government and tax-exempt organization employees to save for retirement. In 2026, the contribution limits for 457(b) plans are changing, which may have a significant impact on individual participant accounts. As we explore the proposed changes and their effects on retirement savings, it’s essential to understand how these modifications will influence individual participant accounts and whether they need to reassess their contributions.

The Internal Revenue Service (IRS) has announced that the 457(b) plan contribution limits for 2026 will be $23,000, the same as the 2025 limit. However, the IRS is proposing a catch-up contribution limit of $7,500 for participants 50 or older, also unchanged from 2025. It’s worth noting that the IRS periodically reviews these limits to ensure they remain aligned with inflation and other market factors.

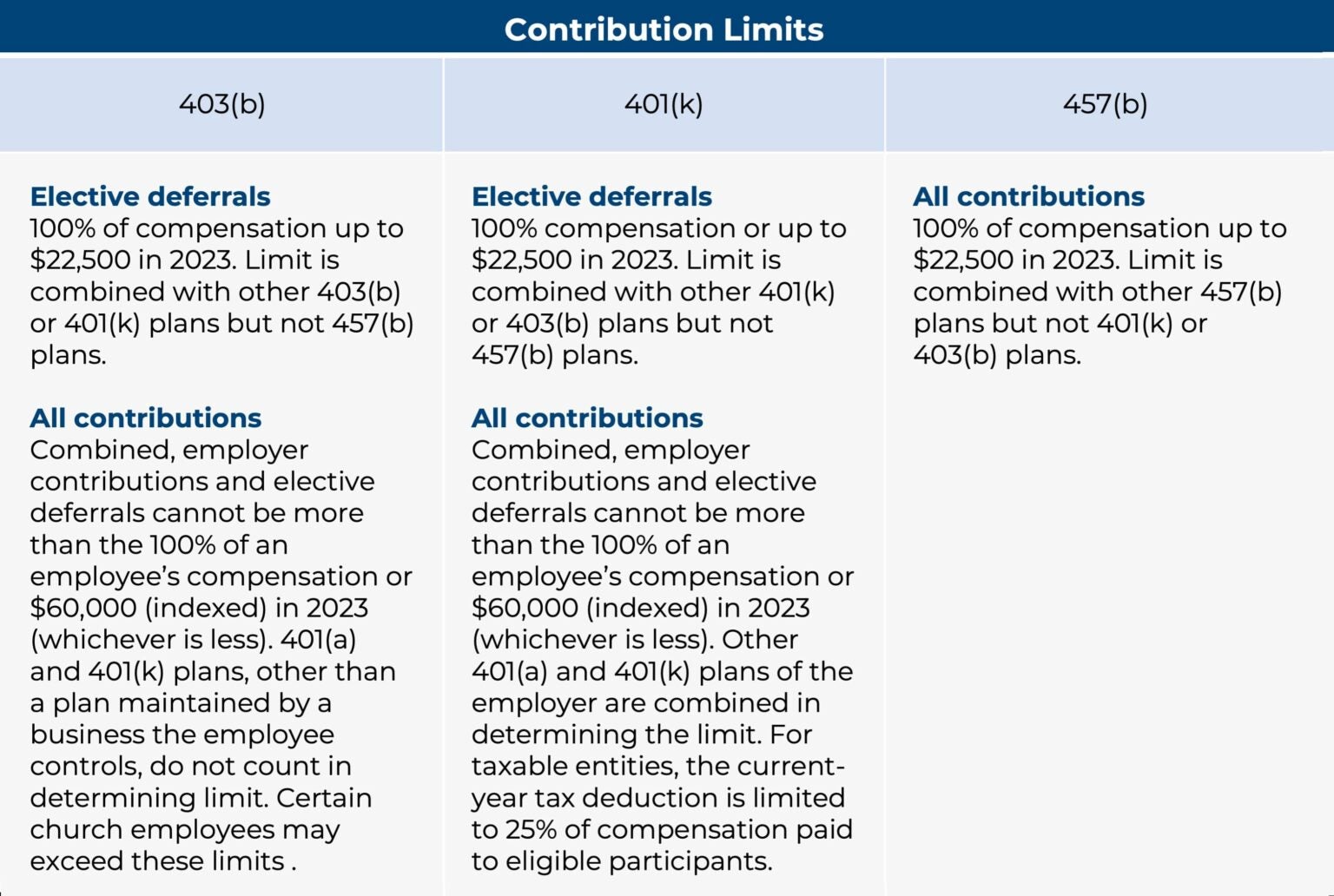

Comparison to Other Retirement Savings Plans

When comparing the 457(b) contribution limits to other types of retirement savings plans, it’s essential to understand the differences between them. For instance, traditional 401(k) plans have a limit of $23,000 in 2026, with a catch-up limit of $7,500 for participants 50 or older. Roth IRAs have a contribution limit of $7,000 in 2026, with a catch-up limit of $1,000 for participants 50 or older. It’s crucial for individual participants to consider these differences when making contribution decisions.

Benefits of Participating in 457(b) Plans, 457b 2026 contribution limits

Participating in 457(b) plans offers several benefits, including:

- High contribution limits: The 457(b) plan contribution limits are among the highest available for retirement savings plans, allowing participants to save more for their future.

- Flexibility: 457(b) plans offer a range of investment options, allowing participants to diversify their portfolios and adjust their contributions as needed.

- Tax benefits: Contributions to a 457(b) plan are made on a pre-tax basis, reducing taxable income and lowering the overall tax burden.

- No required minimum distributions (RMDs): Unlike traditional IRAs and 401(k) plans, 457(b) plans do not have RMDs, allowing participants to keep their savings intact for as long as they want.

Regularly Review and Adjust Retirement Savings Contributions

To ensure they meet their long-term retirement goals, individuals should regularly review and adjust their retirement savings contributions. This involves reassessing their income, expenses, and investment goals, as well as adjusting their contribution amounts accordingly. By staying on top of their retirement savings, individuals can maximize their contributions and build a secure financial future.

457(b) Plan Contribution Limits for Special Employee Groups in 2026

In 2026, employees in special groups, such as law enforcement officers and firefighters, may have unique 457(b) plan contribution limits. Understanding these contribution limits is crucial for retirement savings strategies.

Some special employee groups may have additional or different contribution limits than regular employees. Law enforcement officers and firefighters, for example, may be allowed to contribute more to their 457(b) plans than others.

Contribution Limits for Employees in Non-Taxable Cities or States

For employees living in non-taxable cities or states, such as those with no state income tax, the contribution limits for 457(b) plans may be different. These employees may contribute more to their plans or have different rules applying to their contributions.

Employees in non-taxable cities or states may be able to contribute more to their 457(b) plans because they are not subject to state income tax on their contributions. This can result in lower overall taxes on their contributions and potentially increase their retirement savings.

Impact on Individual Retirement Savings Strategies

The unique contribution limits for special employee groups, such as law enforcement officers and firefighters, can have a significant impact on individual retirement savings strategies. Employees may need to plan accordingly to maximize their contributions and achieve their retirement goals.

Individuals working in special groups or living in non-taxable cities or states should carefully review their 457(b) plan contribution limits and consider seeking professional advice to ensure they are taking full advantage of these opportunities.

Employer-Sponsored Plans and Contribution Limits

Understanding employer-sponsored plans and the contribution limits that apply to individual employee accounts is essential for retirement savings. Employees should review their plan documents and contribution rules to ensure they are in compliance with the regulations and maximizing their contributions.

Employer-sponsored plans, such as 457(b) plans, can provide tax benefits and increase retirement savings. However, these plans also come with rules and contribution limits that employees must be aware of to avoid penalties and ensure they are taking full advantage of the benefits.

Examples and Illustrations

For example, an employee working as a law enforcement officer may be able to contribute an additional $3,000 to their 457(b) plan in 2026, bringing their total contribution limit to $22,000. In contrast, an employee living in a non-taxable city or state may be able to contribute an extra $2,000 to their 457(b) plan, resulting in a total contribution limit of $20,000.

These examples highlight the importance of understanding the unique contribution limits for special employee groups and the potential benefits of these limits. By reviewing plan documents and contribution rules, employees can ensure they are taking full advantage of these opportunities and maximizing their retirement savings.

Special Rules and Considerations

Special employee groups, such as law enforcement officers and firefighters, may be subject to additional rules and considerations when it comes to 457(b) plan contributions. These rules may include requirements for pre-tax and after-tax contributions, catch-up contributions, and in-service withdrawals.

Employees in these groups should carefully review their plan documents and contribution rules to understand these special provisions and how they may impact their contributions and retirement savings.

Real-Life Scenarios and Case Studies

To illustrate the impact of unique contribution limits on retirement savings, consider the following real-life scenario:

John, a firefighter, contributes $15,000 to his 457(b) plan in 2026, taking advantage of the higher contribution limit for firefighters. Through careful planning and contributions, John is able to save an additional $10,000 for retirement, resulting in a total savings of $25,000.

By understanding the unique contribution limits for special employee groups and maximizing their contributions, employees can increase their retirement savings and achieve their long-term goals.

This concludes the information on the 457(b) plan contribution limits for special employee groups in 2026. Employees should carefully review their plan documents and contribution rules to ensure they are taking full advantage of these opportunities and maximizing their retirement savings.

Addressing Common 457(b) Plan Contribution Limit Questions

Plans Explained, Part 3: Rollover Rules for a 457(b) Accounts ...")

When navigating the complexities of 457(b) plan contributions, it’s common to encounter a range of questions and concerns. From income level and employer matching to potential risks and mistakes, understanding the intricacies of contribution limits is crucial for maximizing retirement savings. In this section, we’ll delve into frequently asked questions and provide clarity on the key factors influencing contribution limits.

The Impact of Income Level on 457(b) Contribution Limits

Income level plays a significant role in determining 457(b) contribution limits. As income increases, the number of available contributions may decrease. This is because the Internal Revenue Service (IRS) sets a limit on the amount of income that can be contributed to a 457(b) plan. Understanding how income level affects contribution limits is essential for optimizing retirement savings.

For example, let’s say an individual earns $100,000 per year and contributes 10% of their income to a 457(b) plan. If their income increases to $120,000 per year, the contribution limit may decrease, potentially limiting their ability to save for retirement. By staying informed about income level and its impact on contribution limits, individuals can make informed decisions about their retirement savings.

The Role of Employer Matching in 457(b) Plans

Employer matching is a powerful tool for maximizing 457(b) plan contributions. By understanding how employer matching works, individuals can take full advantage of this benefit and boost their retirement savings. When an employer offers matching contributions, it means they will contribute a certain amount of money to the individual’s 457(b) plan based on the amount they contribute.

For instance, if an employer offers a 50% match on 457(b) contributions, and the individual contributes $5,000 to their plan, the employer will contribute an additional $2,500, for a total of $7,500. Understanding employer matching and its role in 457(b) plans can help individuals make the most of their retirement savings opportunities.

Carefully Reviewing Employer-Sponsored Plans

Carefully reviewing employer-sponsored plans is essential for understanding contribution limits and potential risks associated with high contribution rates. Individuals should take the time to review their plan documents and speak with their employer or a financial advisor to gain a deeper understanding of their 457(b) plan.

Some common risks associated with high contribution rates include:

- Exceeding 457(b) contribution limits, potentially leading to penalties and fees.

- Losing access to employer-matched contributions due to high income levels.

- Inadequate knowledge of plan features and benefits, leading to missed opportunities for savings.

Examples of 457(b) Plan Contribution Limit Mistakes

Examples of 457(b) plan contribution limit mistakes are plentiful, and understanding these mistakes can help individuals avoid similar pitfalls. Some common mistakes include:

- Exceeding contribution limits, resulting in penalties and fees.

- Not taking advantage of employer matching contributions due to a lack of understanding.

- Failing to review and adjust plan contributions in response to income changes or other factors.

Preparing for Potential Changes to 457(b) Contribution Limits

Potential changes to 457(b) contribution limits can have a significant impact on retirement savings. To stay ahead of the curve, individuals should be aware of the following:

- Changes to income limits and their impact on contribution rates.

- Updates to employer matching contributions and their potential impact on retirement savings.

- Advancements in plan features and benefits that can improve retirement outcomes.

457(b) Plan Contribution Limits and Tax Implications in 2026

Participating in a 457(b) plan can have significant tax implications for individuals, and it’s essential to understand how these implications can impact your retirement savings strategy. In this section, we’ll delve into the tax implications of 457(b) plans, including potential deductions and tax savings.

When you contribute to a 457(b) plan, you may be eligible for tax deductions, which can help reduce your taxable income. As of 2026, the deductibility of contributions to a 457(b) plan depends on your income level and other factors. It’s crucial to understand how these tax implications can affect your individual situation.

Tax Implications Based on Income Level

—————————————-

Income level plays a significant role in determining the tax implications of participating in a 457(b) plan. If you’re a high-income earner, you may be subject to different tax rules and regulations. Conversely, lower-income individuals may benefit more from tax deductions. To illustrate this, let’s consider a few examples of income levels and their corresponding tax implications.

| Income Level | Tax Implications |

| — | — |

| Low-income (< $50,000) | Eligible for tax deductions, reducing taxable income |

| Middle-income ($50,000-$100,000) | Eligible for tax deductions, but with limited benefits |

| High-income (>$100,000) | Subject to different tax rules, potentially reduced tax savings |

In the table above, we’ve provided a simplified breakdown of how income level can impact tax implications. Keep in mind that individual circumstances and factors can influence these outcomes.

Understanding Tax Implications and Creating a Comprehensive Retirement Savings Strategy

—————————————————————————————–

As you can see, understanding the tax implications of 457(b) plan contributions is crucial for creating a comprehensive retirement savings strategy. Factors like income level, tax deductions, and other variables can significantly impact your tax situation. To get the most out of your 457(b) plan, consider consulting a financial advisor or tax professional to optimize your contributions and minimize tax liabilities.

Ending Remarks: 457b 2026 Contribution Limits

Whether you’re a law enforcement officer, firefighter, or any other special employee group, it’s essential to understand your 457(b) plan contribution limits and how they impact your retirement savings. By regularly reviewing and adjusting your retirement savings contributions, you can ensure you meet your long-term goals and maximize your 457b 2026 contribution limits. Stay ahead of the game and make the most of these crucial contribution limits.

Helpful Answers

What is the maximum contribution limit for 457(b) plans in 2026?

The maximum contribution limit for 457(b) plans in 2026 is subject to change, but it’s generally around $20,500. However, this limit may vary depending on your income level and employer’s plan.

Can I contribute to 457(b) plans and other retirement accounts simultaneously?

Yes, you can contribute to 457(b) plans and other retirement accounts, such as 401(k) or IRA plans. However, the total contributions you make in a year across all accounts cannot exceed the annual limit set by the IRS.

How do income level and tax implications impact 457(b) contribution limits?